Open Banking APIs: Real Integration Complexity

Open banking sounds simple, but API reliability varies by institution, data formats differ wildly, and transaction categorization is accurate 73-92% of the time. This is what integration actually looks like.

Open banking sounds simple: banks expose APIs, you connect to them, users share their financial data. The marketing materials from Plaid, Yodlee, and others make it seem like a weekend project.

The reality is messier. API reliability varies by institution. Data formats differ wildly across banks. Transaction categorization is accurate 73-92% of the time depending on the provider. Connection maintenance requires ongoing engineering attention, not a one-time integration.

The Promise vs. The Reality

Open banking emerged to solve a real problem: screen scraping. Before APIs, fintech apps obtained bank data by literally logging into bank websites with user credentials and extracting data from HTML pages.

Screen scraping had serious issues: security risks (users shared banking passwords), fragility (website changes broke integrations), legal uncertainty, and data inconsistency.

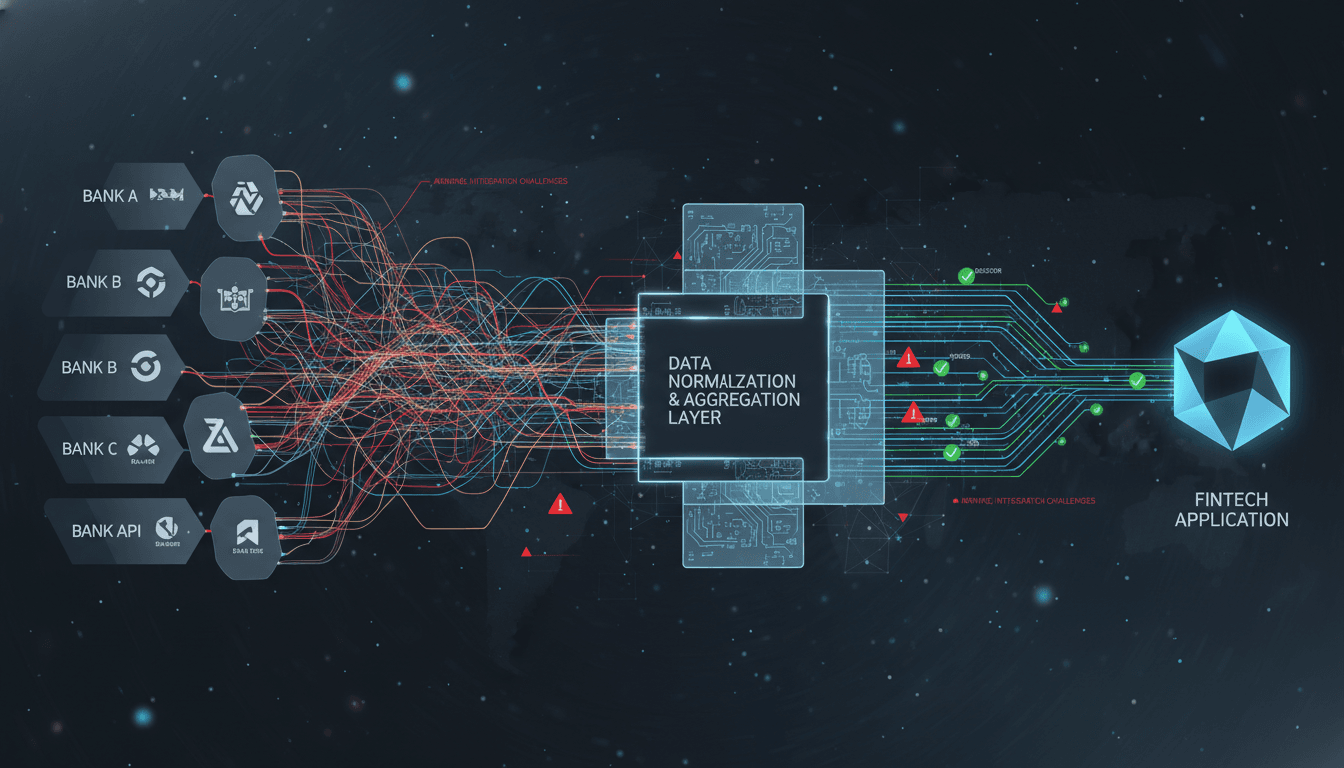

The Data Normalization Problem

The fundamental challenge with open banking isn't connecting to banks. It's making sense of what comes back. A single coffee purchase might appear as five completely different formats across banks. Your application needs to understand these are all the same thing.

Data aggregators provide merchant identification and categorization, but accuracy varies: 73-92% depending on provider. That 80% accuracy sounds good until you realize 20% of transactions in a budgeting app are wrong.

API Reliability Is Worse Than You Think

Average response times range from 200-600ms typically, but can reach 2-5 seconds for slow institutions, 10-30 seconds during degraded states, or immediate failure during complete outages. Your UX needs to handle all of these gracefully.

Bank connections break for many reasons: user changes password, bank updates authentication flow, MFA requirements change, OAuth tokens expire. Plan for 1-5% of connections needing re-authentication monthly.

The Provider Landscape

Plaid is the dominant player for US consumer fintech with 12,000+ institutions and excellent developer experience. Yodlee (Envestnet) is enterprise-focused with 20,000+ global institutions. Finicity (Mastercard) focuses on verification and lending use cases.

Regulatory Complexity

UK and Europe have PSD2 with mandated bank APIs. The US has CFPB Rule 1033 finalized in October 2024 but currently in litigation. Multi-region products need different integration approaches per market.

Architecture for Open Banking

Never block user actions on real-time bank data fetches. Use asynchronous data retrieval with background sync and incremental updates. Build robust webhook handling with idempotency, retry queues, and monitoring.

Cost Realities

Typical aggregator pricing: Plaid $0.30-$1.50 per connection per month, Yodlee enterprise contracts at $0.10-$0.30 at high volume. At 10,000 connected users, you're looking at $36,000-$180,000 annually just for bank data access.

Initial integration costs $10,000-$30,000 for proper implementation. Budget 2-3x your initial estimate for integration. Edge cases dominate the work.

Key Takeaways

Data normalization is the hard part: Transaction descriptions, account types, and balances require significant mapping work.

Reliability varies by institution: Design for degraded states, not just happy paths.

Categorization is good, not great: Expect 73-92% accuracy out of box, plan to improve it.

Costs add up: Per-connection fees, integration, and maintenance are material expenses.

The fintech products that succeed with open banking take integration seriously. It's not a commodity API call. It's a core architectural concern that affects user experience, reliability, and unit economics.